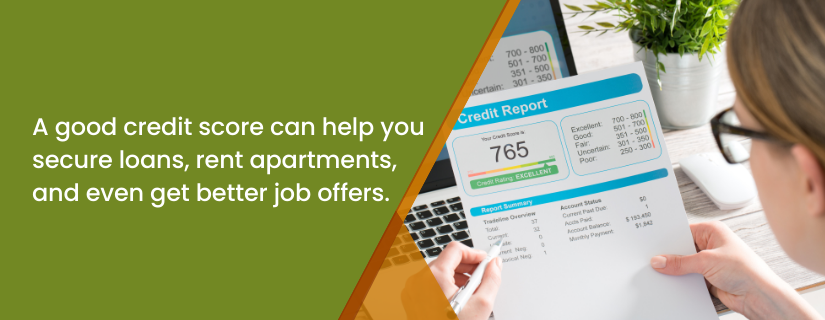

A credit score can have a dramatic impact on your life. This includes your ability to obtain a mortgage or a lease, your ability to find a job, your insurance premiums, and your cost of borrowing money.

At First Exchange Bank, we deal with credit scores and credit reports all the time so we’re frequently asked for credit-building tips, how to fix a low credit score, how to build credit, and the best ways to improve a credit score.

With that in mind, we offer this explanation of what a credit score is, how it’s calculated, and some credit score improvement strategies for 2025.

What Is a Credit Score and How is it Calculated?

A credit score, also known as a FICO score, is a number that credit reporting agencies use to indicate how likely you are to pay your bills on time, including loan payments.

Ranked in order of importance, a credit score is affected by your:

- Payment history (35%)

- Credit utilization, or the difference between your available credit and what you owe (30%)

- Length of credit history (15%)

- Recent loans or credit card applications (10%)

- The type of debt you have: credit cards, mortgages, auto loans, etc. (10%)

Why Is My Credit Score Important?

Your credit score has a direct impact on your access to loans and credit cards, your employment, your ability to sign a lease, and to qualify for insurance. Banks, insurance companies, and employers view your credit score as a sign of how risky a customer or an employee you are.

A low credit score can lead to increased insurance premiums and higher interest rates on loans and credit cards. However, at First Exchange Bank, we do not determine loan interest rates based on credit scores. Additionally, landlords often perceive a low credit score as an indication of you might not make rent payments on time.

While employers cannot see your actual credit score or your annual income, they can learn how much debt you have and your payment history, any bankruptcies you’ve had, your name and address, and possibly your past and current employers. A credit report can also include legal judgments and fines, such as a judge issuing a civil penalty against you.

How Can I Check My Credit Score?

There are a couple of ways that you can check your credit score and your credit history.

Many credit card companies let their customers check their own credit score on a monthly basis for free. You can also check any credit or loan statements to see if they include your credit score.

There are three credit reporting agencies in the United States: Equifax, Experian, and TransUnion. Federal law allows you to get a free credit report once a year from each of these, which you can obtain by visiting AnnualCreditReport.com.

Your free credit report will not include your credit score, although you could set up an account with one or more of these credit agencies that lets you monitor your FICO score. They might offer you a subscription service to monitor your credit, although it’s not required to obtain your annual credit report.

Keep in mind that each of these credit agencies have slightly different ways of calculating your credit score, so you won’t get exactly the same score from each agency.

It’s a good idea to check your credit history every year, to make sure it’s accurate and verify what kind of debt you have. You may have an old forgotten credit card account that still exists. You can also look for any signs of identity theft or fraud. If a scammer took out a loan or credit card in your name, this should appear in your credit report.

How Can I Improve My Credit Score?

Just as it’s a good idea to check your credit score once a year, it’s also important to dispute any missing or inaccurate information by contacting whichever agency has this information in your report, and the lender or financial institution involved. If your credit report includes an outstanding balance on an account that you paid off or closed, this can have a negative impact on your credit score so it’s important to get that resolved.

Here are some of the best ways to improve your credit score and the most effective credit habits for 2025:

Pay Your Bills on Time

Because your payment history is typically the most important part of your credit score, paying all your bills, credit cards, and loans on time is crucial for maintaining good credit. Even if a payment is late by just a few days, it can still affect your score.

Any bills sent to a collection agency can dramatically affect your credit, and this information will remain on your credit report for seven years.

You might consider enrolling in automatic payments for things like mortgages and credit cards, although you’ll have to make sure you always have enough funds in your checking or savings account to cover these bills.

Another option is to contact your creditors or consult a credit counselor. If your bills include substantial medical debt, you might speak with your medical provider’s billing department to see if they offer financial assistance or if can put you on a payment plan.

It’s worth noting that medical debt will only affect your credit score if the balance is more than $500 and is more than a year old. Any medical debt that’s sent to a collections firm will still show up in your credit report, so it’s important to get any debts resolved before that happens.

Reduce What You Owe

Your credit utilization is the second key factor that affects your credit score. This includes your credit card and any revolving lines of credit you may have, such as a home equity line of credit (HELOC).

The closer your outstanding balance is to your total credit limit, the more negatively it’s going to impact your credit score. Keeping your credit usage at less than 30% of your credit limit can significantly improve your credit score.

If your debt load is higher than this, focus on reducing what you owe as much as possible. Start by paying off your debts that carry the highest interest first, while you continue making the minimum payment on your other credit cards and debts. For more advice on this, check out our blog post on How to Pay off Debt Faster.

Use Credit Cards to Boost Your Score

Because your debt-to-credit ratio has a tremendous impact on your overall credit score, these credit card tips for building credit in 2025 can go a long way to improving your credit score.

Asking your credit card company to raise your credit limit might have a slight negative impact on your credit score for a month or so, but it can improve your credit score in the long-term as long as you don’t actually use this as an opportunity to increase your amount of debt.

If your income has increased over the previous year, or you’ve maintained a good payment history on all your bills and loans, you’ll have a good chance of getting your credit limit increased. Some credit card companies allow you to ask for an increase once every six months.

For any credit cards that you don’t use very often, it’s a good idea to hold on to them and keep them active, because they contribute to your amount of available credit and help your credit score.

At the same time, you should avoid opening new credit cards just to increase your available credit because opening new lines of credit can negatively affect your credit score.

Avoid Going into Collections

Any unpaid debt that you have could wind up being sent to a collection agency. If this happens, it could have a significant impact on your credit score.

If you’re at risk of any debt going into collections, try to work out a payment plan with your creditor before this happens. If any unpaid debts are sent to a collection agency, focus on paying this off as soon as possible.

Debt collectors are required to try and contact you over the phone, through the mail, or electronically and to give you time to respond before they notify credit reporting agencies. If you are contacted by a debt collector, it’s important for you to respond and get your debt settled before this happens.

Of course, there are fraudsters out there who might falsely claim that you owe someone money, so it’s important to make sure this person and their company are legit before offering them payment.

If an unpaid debt winds up on your credit report, you might ask the collection agent to remove this information from your report once your debt is paid off.

We’re Here to Help

At First Exchange Bank we’ve served the communities of North Central West Virginia for more than 90 years. If you need more information on how to improve your credit score, or would like to learn more about our excellent banking and services, please contact us or stop by one of our seven locations.